Change your processing platform to Way4 and create new revenue streams

MaaS Global, the provider of all-inclusive mobility app Whim, partnered with Enfuce to launch a card payment offering. Whim app users can receive a virtual Mastercard prepaid card and make mobile payments for public transport, taxis, rental bikes and cars, and other options. These open-loop cards can also be tokenized for use via Apple Pay, Samsung Pay and Google Pay.

Rocker, the Swedish fintech startup, chose Enfuce to issue feature-rich cards compatible with any currency or geography. This aligns with Rocker’s plans to expand its business throughout Europe.

Jysan Bank in Kazakhstan, who works directly with OpenWay, promotes multi-currency cards with cashback as a savings instrument. Its card product combines many accounts in different currencies linked to the same card. The card is replenished with cash or via money transfer. Customers can choose between 16 currencies and move funds between them via online banking anytime. This enables them to respond quickly to FX fluctuations even during the pandemic, when many bank branches and foreign exchange kiosks are entirely closed. When the lockdown ends, Jysan Bank cardholders will probably have developed two habits around the multi-currency card. They will use it to make payments abroad, and for managing savings at home.

Multi-currency cards are also great for attracting new clients. For example, National Bank of Oman offers prepaid contactless multi-currency cards ‘Badeel Travel’ to any Omani resident. It supports conversion of Omani rials into US dollars, euros, British pounds, Swiss francs, Indian rupees, Thai bahts, United Arab Emirates dirhams, and Saudi riyals.

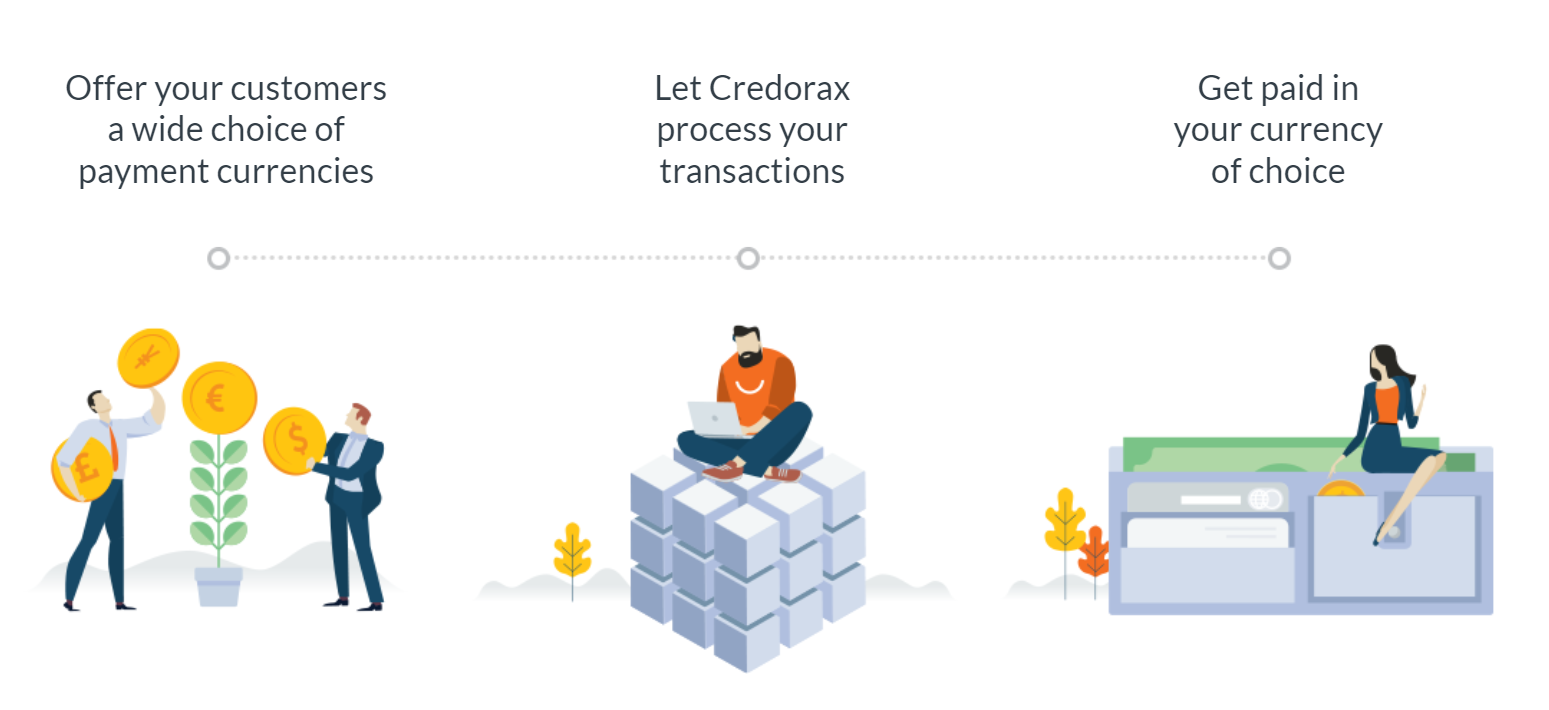

Credorax (now part of Shift4) is one of the most successful cross-border e-commerce acquirers who uses Way4 to power DCC and MCP. This acquirer reports a CAGR of over 52%. Its website proudly says to the merchants: “Get paid in your currency of choice. Process in over 100 currencies”.

Pleo, a Danish fintech company, partnered with Enfuce to innovate its business spending platform. The startup provides 5,500 businesses across six countries with smart commercial company cards and automated expense reporting. Enfuce was chosen to ensure that Pleo cards work anywhere and anytime as the startup rapidly expands across Europe.

Lotte Finance Vietnam is one of OpenWay’s clients who offer and issue loans instantly at the moment of purchase. Typically, this would be an instalment product, but Way4 also allows loans to be configured as charge account. The loan can be bundled with a payment card which customers can use in the future for various payments and transfers.

Indo, Iceland’s first challenger bank, chose Enfuce as its issuing processor and provider of innovative plug-and-play carbon footprint tracker. Indo cardholders can track monitor the CO2 emissions of their individual spending in categories like food and transportation, get actionable insights on sustainable lifestyles and improve their consumption habits accordingly.

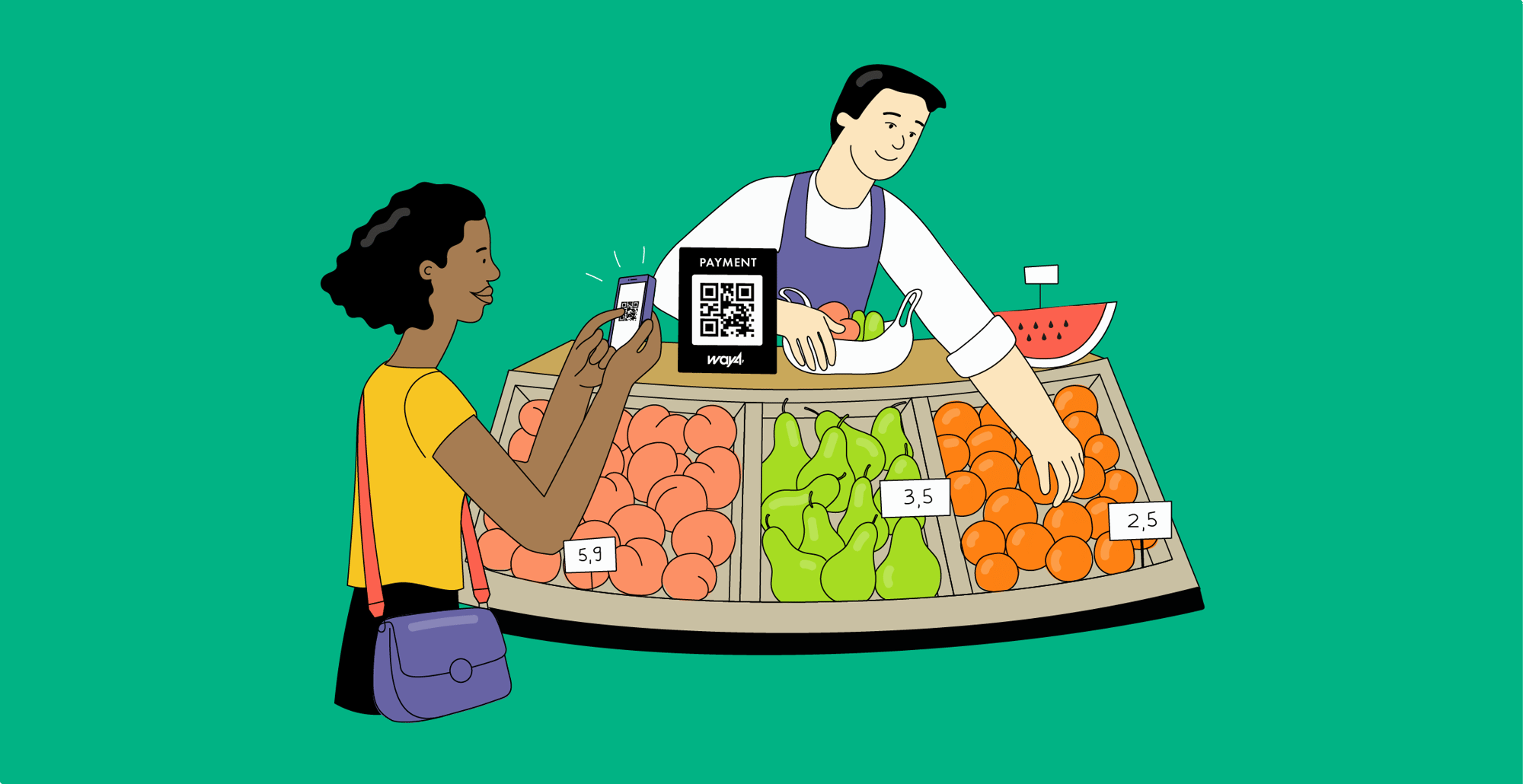

Halyk Bank in Kazakhstan has been relying on OpenWay’s issuing and acquiring innovations for fifteen years. In 2018, it introduced VISA Scan&Pay QR code service, which boosted its expansion into the SME and transit market.

SmartPay, a Vietnamese fintech brand, has partnered directly with OpenWay to build a very successful mobile wallet ecosystem. Launched in May 2019, it developed rapidly within a single year and enrolled more than 1,000,000 consumers and 100,000 merchants across the country.

⨉