Prepaid cards: multi-case study

How prepaid cards can help banks to grow despite the pandemic

Some B2B customers appear to be the most promising for adopting new prepaid products. Projects targeting government, retail, and corporate segments are expected to enjoy an even higher growth rate than issuance of general-purpose prepaid cards. Transport-related projects seem attractive as well.

This multi-case study explores how issuing banks and processors can make successful prepaid products for governments, transport authorities, retailers, and corporates. What technologies and business advantages are needed to launch viable and profitable solutions? Here is the overview of best practices.

Table of contents

Click on a header to skip directly to that section.

Deliver government assistance safely and efficiently with prepaid cards

Many governments this year have responded to the global pandemic by distributing large volumes of aid packages quickly and securely. Some authorities have transferred up to $1,400 to the affected citizens as one-time payments, while in other countries, aid payments have been recurring since the start of the pandemic. With lockdown restrictions and hygienic recommendations, contact-free delivery of funds is the best option. Many governments are commissioning prepaid cards to support their citizens with no exclusion for the unbanked. What requirements do such cards have to meet?

Allow beneficiaries to receive aid with no delay, no charge, and less health risk

Instant disbursements and immediate access to funds are the first criteria that a prepaid card commissioned by the government has to meet. Italian municipalities, for example, chose Soldo Care cards to distribute financial support to more than 20,000 families. Recipients could use the cards immediately at any merchant that accepts Mastercard payments.

Despite its convenience, the instant disbursement feature is not quite common for such projects. For example, in the US it is available to only 13% of private consumers and 8% of microbusinesses.

To achieve social objectives, prepaid cards should have no service charges. Soldo Care cards used by Italian authorities meet this requirement. They allow free-of-charge reloading, which is beneficial for unbanked recipients who can continue using the card for their needs. No part of the aid budget is diverted to the payment of fees, which means the government can spend money earmarked for recipients more effectively.

Contactless payments make prepaid cards safer than cash in terms of hygiene. Financial aid recipients often belong to the most vulnerable groups during an epidemic, such as senior citizens, who face restrictions on movement. That is why many governments are switching to contactless prepaid cards to distribute regular welfare payments. In Chile, for example, social services are going to issue 400,000 prepaid cards for pensioners and low-income earners by the end of the year.

Provide governments with full control of disbursements to reach social objectives

A prepaid card platform must be agile, since authorities may need to quickly adapt the basic infrastructure to the local budget, types of beneficiaries, or terms of prepaid card use. In Italy, the Soldo Care prepaid card was first rolled out by the Municipality of Milan, then 21 more regions joined, adapting the prepaid card to their needs.

Prepaid cards are usually issued with geographic and time limits on prepaid card use. The British island of Jersey, for example, commissioned 105,000 prepaid cards for £100 each which could be used for purchases exclusively at local businesses until October 31, 2020. In this way, the local government aimed to support the island’s inhabitants and spur economic activity. Such restrictions allow governments to control the use of funds: prepaid cards containing childcare payments may only be accepted in baby stores, and student cards containing educational loans may only be used to pay in university offices.

The security of the platform is critical for the government and the issuing bank. More and more cards are equipped with the biometric identification feature, as one of the strongest methods of fraud protection. In Iraq, for example, the state has suffered financial losses from people using fake IDs to receive illicit monetary support meant for state employees and welfare allowance recipients. To stop fraudulent transactions, the country is adopting a biometric ID system and has introduced the national QI Card with embedded fingerprint data. Biometric identification takes place at every payment, including transactions with prepaid Qi Cards.

The above-mentioned features are the top requirements for a prepaid card serving a government project. They can be all met with Way4 Social Cards, a flexible payment software solution from OpenWay. It allows an issuing bank to adapt an existing card product or create a new one from scratch to fit the needs of a particular project, region, or type of beneficiaries. Besides prepaid cards, the Way4 Social Cards solution allows institutions to issue credit and debit cards for individuals and businesses.

Governments and social organizations often lack access to reliable state-of-the-art financial technologies as they don’t always have enough funding or banking expertise. Way4 eliminates this obstacle, allowing banks to deliver an affordable, yet secure and modern payment product to governments and social organizations. Way4 Social Cards is part of the same platform that powers issuing of commercial cards, so it enables the same high level of fraud protection and the same stack of payment innovations.

Make interoperable and marketable prepaid solutions for transport

This year has shown how quickly transport consumption trends can change. Remember how before the pandemic, ecologically engaged individuals and city authorities promoted the use of public transport over privately-owned vehicles? This year, the situation has turned upside down. First, we observed a natural decrease in mobility during lockdown. In the French city of Lyon, for example, only 4% of citizens were moving around the city at the end of March, when mobility restrictions were set in action, compared to 86% two weeks earlier. Now many regular commuters are rejecting public transport and opting for private vehicles instead. It looks like only ride-hailing, conventional taxi, car sharing, shared e-bikes, e-scooters, and e-mopeds have remained almost at the same level during the pandemic.

Under these unstable conditions, is it sustainable to create a prepaid card for transport? The answer can be yes, if an issuer implements some of the ideas below.

Create a prepaid product compatible with several means of transport

The brightest example is an all-inclusive transport app named Whim, supported by the cloud-based processor Enfuce. Whim users can top up their virtual prepaid card and benefit from pay-as-you-go plans in five European countries and Japan. Whim supports payments for public transportation, railway trips, taxi rides, car hires, shared bikes and e-scooters, and even a ferry. There is also an option to buy a multi-modal virtual subscription on a specific set of public and private transport services. For example, Whim users can opt for daily commuting or solely weekend trips. This flexibility makes Whim’s offer sustainable despite travel restrictions or consumer preferences as it is up to customers to decide when and how they are going to use their prepaid trips or loaded money.

In the three years since launch, Whim users have completed over eight million trips, and now the mobility-as-a-service app is aiming to get even broader coverage with its new open-loop prepaid Mastercard.

Launch into a well-developed and regulated market

Success of a transit prepaid card depends a lot on how the transport infrastructure is organized in a particular country. Compare the two examples below.

In Kenya, a major part of the public transport is privately owned. When the government required this industry to migrate to cashless, operators of matatus (local private buses) sabotaged the initiative. They kept asking passengers to pay with cash because their Android phones needed to process non-cash transactions were allegedly “lost” or “broken”. The truth was that cashless payments made their daily earnings too transparent and prevented them from raising fares arbitrarily. There was too little benefit for private transport owners and operators, so in the end, the government initiative crashed.

In Hong Kong, by contrast, the transport infrastructure had already been well-developed and mostly state-owned by 1997 when the Octopus Card was introduced. It was the second contactless smart card in the world that worked exclusively as a transit card. Now more than 95% of the Hong Kong population owns an Octopus Card, and it has even grown into an open-loop card.

It is no surprise that prepaid card issuers have a better chance of success in a more stable market in control of the government.

Provide exclusive access to transport services

In the segment of prepaid cards for transport, competition may be fatal. The situation with the chaotic transport system in Kenya was compounded by the fact that several issuers distributed transit prepaid cards. They were tied to different bus lines, and passengers had to wait until the car accepting exactly their type of card arrived. It wasn’t convenient for customers, neither was it profitable for the prepaid card issuers, who only managed to hold a small share of the market each.

Sometimes an issuer can offer a clever solution to occupy a market niche. In Argentina, all local banks were eliminated from the competition for Uber transactions in one day. The court had accused Uber of violation of local transportation and labor standards and prohibited the service from accepting payments made by debit and credit cards issued in Argentina. Uber obeyed the court’s decision — and pointed out to their customers that they could still use the prepaid cards registered abroad. The company partnered with Xapo, a bitcoin prepaid card issuer based in Hong Kong, and provided a $30 discount to passengers paying with their cryptocurrency cards.

Include the features to benefit transport owners and passengers

Convenience for both transport service providers and final customers is crucial for a transport prepaid card to succeed. The Octopus Card, for example, managed to grow into a full-pledged prepaid card thanks to its initial benefits for cardholders. It is easy to reload and connect Octopus to other credit or debit cards, it comes in physical and virtual formats, and it even allows passengers to take one trip when their balance is less than a transport fare. The card can be used for identification to access secure areas — provided cardholders have required this option, because by default, the card is anonymous.

For the merchants that accept Octopus as an open-loop card, it is profitable because it offers competitive card acceptance fees and next-day settlement, and its technology is compatible even with parking meters. As a result, there are more than 37,000 retail outlets in Hong Kong who accept this card, and Octopus daily transactions average HK$14.9 million.

The speed of transactions is critical for transit prepaid cards. No passenger wants to wait in line while somebody else’s fare is being authorized, and no transport owner wants to experience any delays because of it. To provide instant access for regular transport users, there is the fast-track technology available on the Way4 platform. The technology is now being implemented in the subway of one European city.

Transit merchants can set rules of micro-payment aggregation to collect transactional data during a chosen period of time and send it to the IPS in a batch. This way, they save on the fees for sending and processing each transaction separately.

To sum up, a prepaid card for transport can be the most successful when it is accepted on various means of transport, including the ones most in demand. A popular transit card can even grow into an open-loop prepaid product, like the Octopus Card and the Whim app. An issuer can improve its position by improving their product with unique and flexible features, available on Way4.

Launch a co-branded prepaid product with a retailer

In 2020, retail revenue volumes have taken a real tumble. They will only return to normal in the middle of 2022, according to US statistics. Retailers are in desperate need of funds to tide them over until sales levels normalize. How can banks and fintechs help them to increase their income?

Some retailers benefit from prepaid cards, accepting them as no-interest loans from their customers. Starbucks is the best example: their stored value card liability and current portion of deferred revenue in 2019 reached $1.269 billion. To compare, 102 financial institutions in the US have domestic deposits of less than $1 billion. The funds loaded on Starbucks Cards generate yearly income to the company: according to the company’s spokesperson, 97–98% of the loaded deposits is redeemed. Although the stored funds on the cards don’t have an expiration date, the company keeps track of the so-called breakage amounts — the funds that were loaded on prepaid cards but never used. The amount is counted as a proportion of redemptions made over the recent year and those of the past, and these can reach $125.1 million in company-operated store revenues and $15.7 million in licensed store revenues, according to data from 2019. Starbucks hasn’t announced any plans for entering the finance industry, but banks are already expressing their concerns.

This case shows that retailers can succeed in managing card products on their own, and financial institutions may easily lose potential revenue. To avoid this, banks can offer mutually beneficial partnerships to retailers and issue co-branded prepaid cards.

Choose a promising co-branding partner

Idea number one is to find a retail niche where no direct competitor has a prepaid product yet. The strategy worked well for Starbucks: their closed-loop plastic was a pioneer of stored-value cards, and their mobile app was the first-ever exclusively created for a payment card. They were early to introduce an in-store mobile wallet supporting the Order and Pay feature and invisible payments. With this feature, customers make orders in the mobile app and pick up the chosen goods at a physical Starbucks counter. The payment happens automatically and seamlessly for the consumer: the money is charged from the integrated prefunded account, a debit/credit card, or a PayPal account. Now the in-app payments are making up 12% of the company’s transactions in the US with more than 25 million customers having used the feature. Cryptocurrency payments are also currently being tested in the app.

Another promising idea is to partner with a second-to-market player that needs to grow its revenues and market share to catch up with the first mover. To achieve their goals, such retailers may accept a co-branded prepaid offer coming from an experienced issuing bank.

In both cases, launching co-branded prepaid products with grocery stores, restaurants, and coffee shops shows promise. Such cards have enjoyed the biggest share in the global purchase volume of prepaid card payments — 47.62%, reaching $208 million in 2019, and they are expected to stay on top until 2026.

Offer a prepaid product that retailers can’t manage on their own

A retailer may lack the expertise for launching a more complicated prepaid product, or not have a banking license. A bank can step up and offer a co-branded open-loop card, for example. This is what Chase has done for Starbucks: together, they have issued a reloadable open-loop Visa prepaid card. This way, Starbucks can provide their loyalty rewards at a broader range of merchants, and Chase has gained a partner whose brand will expand the bank’s customer base and promote more active use of the prepaid cards.

An experienced issuer can help a retailer to create a custom prepaid solution. Shared expertise can result in higher potential profits and brand awareness. For example, Barclays provided Costa Coffee with its bPay by Barclaycard technology to make the UK’s first reusable contactless coffee cup together. It worked as an open-loop prepaid product that could be used for payments in the café chain and at other merchants, including even the underground. The contactless payment element was simply integrated into existing reusable cups.

The project received publicity from major outlets specialized in finance and marketing — Finextra, FinTech Futures, FMBE, and Mobile Marketing. The co-branded innovation was successful primarily as a promotional tool, one of the objectives that an issuing bank can reach through a joint prepaid project with a retailer.

Leave out irrelevant features and communicate the prepaid card’s value clearly

It is critical to ascertain that a prepaid card addresses end-user needs. Think of Carrefour, which had to terminate its C-zam offer three years after the start. They had planned to acquire two million prepaid cardholders by 2022, but never approached this number. Was C-zam too complicated? Perhaps it was, especially since customers had to sign up to an online-only bank account. Carrefour shoppers might have only needed a simple prepaid card with no registration.

Communication with potential and actual prepaid cardholders matters. C-zam prepaid cards were distributed at more than 3,000 points of sale; however, it seems cashiers were poorly informed about the C-zam usage, and customer service was often unreachable. As a result, 30% of the purchased prepaid cards were never activated. Neither widespread awareness of the Carrefour brand as a supermarket nor the corporation’s experience in finance helped their prepaid product to succeed.

It appears to be that prepaid cards may be too complicated for many retailers. They need the expertise of banks to launch and manage card products. Issuers can help by offering a co-branding partnership and prepaid solutions that adapt to each retail vertical’s specifics.

Help businesses to deliver payrolls and control corporate expenses in real time

The corporate segment of the prepaid cards market is growing slower than was predicted. Under normal conditions, the global purchase volume in the corporate cards segment would be expected to more than double in just six years and reach $732 billion in 2026. In that scenario, the percentage of corporate cards on the global prepaid market would even exceed the share of general-purpose prepaid cards issued and distributed by banks.

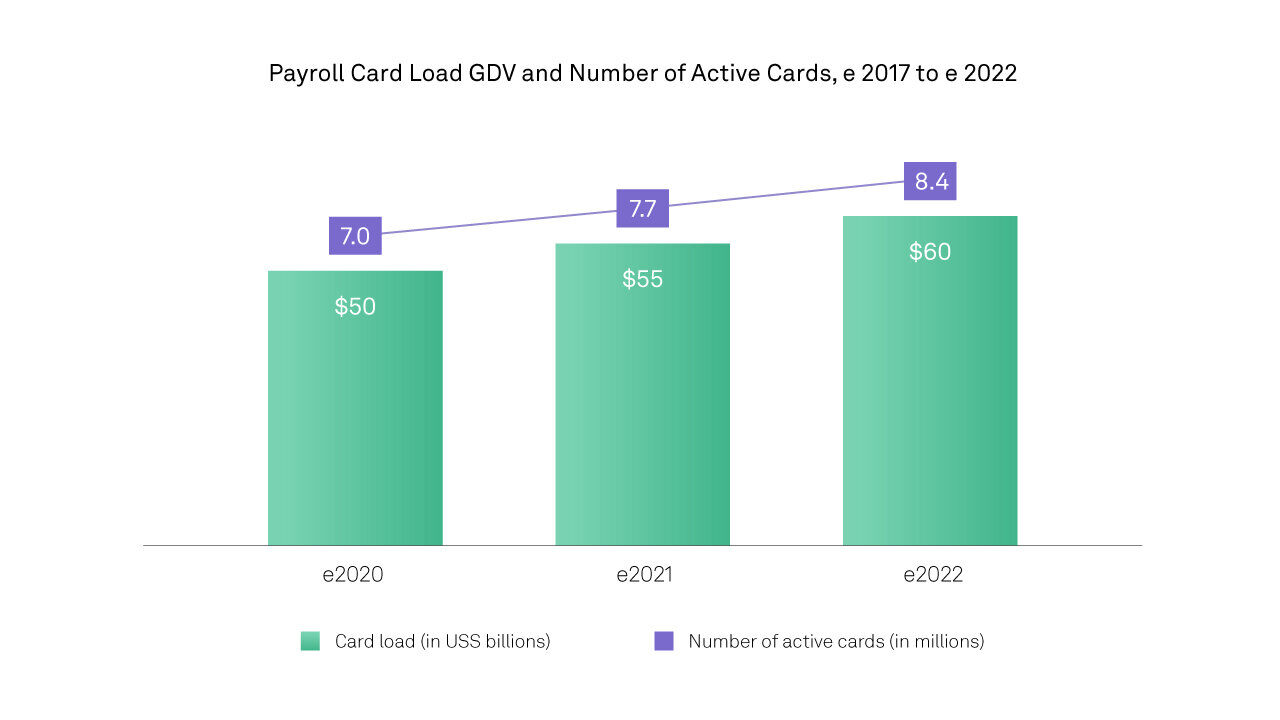

In the US along, payroll cards were forecast to grow and deliver the total sum of $60 billion to 8.4 million workers in 2022.

The pandemic has adversely affected this growth. In 2020, the entire prepaid cards market is estimated to grow only half as fast as last year globally. The total number of payrolls decreased by 19 million payments from March to September 2020.

However, even now, there are some favorable conditions that can support corporate prepaid cards growth. In one part of the world it’s the gig economy, while in others, it’s legal regulations that are improving the position of prepaid cards. For example, in India, the central bank has permitted businesses to deliver incentives and salary disbursements through prepaid cards. As a result, the country has seen a 438% increase in the number of prepaid cards.

In any case, a corporate prepaid card has to be flexible to fit the needs of a particular employer and responsive to the changes in the economy so that businesses and employees feel protected against instability. How can a prepaid card issuer meet these requirements?

Facilitate international business connections with a multi-currency option

At the start of the pandemic, when the borders shut down for the first time, many companies found that their employees were stranded abroad. Businesses could have supported them by transferring funds to their prepaid cards with a multi-currency feature. An employer could have calculated an outgoing payment in the company’s home currency, and abroad, an employee would have paid in the currency of a country where they stayed. At that, they would avoid unfavorable exchange rates and extra fees.

An example of an issuer that can help in a similar situation is Enfuce, a cloud-based processor using the Way4 platform. Because of its cloud-native properties, Enfuce can easily adapt a prepaid product to regional or industry specifics and launch it quickly wherever the client is located.

The use of prepaid cards with the multi-currency feature empowers a business to choose the best contractors, suppliers, and partners, no matter where in the world they are located. For such cards, Way4 can be configured to apply a locked-in exchange rate. It allows a corporation to avoid the extra expense of conversion fees.

Enable real-time and instant features for the new generation of clients

The quicker a prepaid card payment goes through, the more attractive the card becomes to consumers, whether they are digital natives or first-time users. One of Enfuce’s clients is Pleo – an issuer of corporate prepaid cards. It offers an instant virtual prepaid card that allows employers to track corporate expenses in real time. A manager receives a notification on their phone every time an employee uses a card, then the transaction is added and categorized automatically on an online dashboard. So far, Pleo has served over 5,500 business customers in six countries and is preparing for further expansion.

Consider the needs of unbanked and underbanked employees

Corporate prepaid cards with flexible features can encourage financial inclusion. Imagine a company whose employees are mostly unbanked — for them, payroll cards can secure timely and convenient payments. But this is just the basics that any prepaid card can provide. To make an outstanding corporate prepaid offer, an issuing bank may add an extra feature — the flexible spending account. It allows employees to put a part of their income aside, keep it tax-free, and use it to reimburse costs of medical services. The feature can be built on the OpenWay’s Way4 platform that analyzes retail transactions and, according to the purchased product code, withdraws the needed amount from a taxed or a tax-free balance.

Way4 can help issuing banks to meet the requirements of all types of prepaid card commissioners. Governments and welfare organizations may rely on customized prepaid products to distribute financial aid in a timely and secure way. Health risks related to in-person cash payments can be minimized, even while using public transport. Retailers can pursue their brand awareness and revenue objectives with unique co-branded prepaid products, and businesses get to control their expenses and payroll transfers in real time.

If you’re seeking an experienced partner for prepaid card issuing, the OpenWay team is at your service. Contact us to learn more about the Way4 Issuing solution, and let’s create the next great prepaid product together!

Learn more: analytic reports, news and case studies

-

“Global and China Prepaid Credit Card Market Insights, Forecast to 2026”. Maia Research, 2020. www.absolutereports.com/global-and-china-prepaid-credit-card-market-16370840.

-

“Prepaid Card Market: Global Opportunity Analysis and Industry Forecast, 2020–2027”. Allied Market Research, 2020. www.alliedmarketresearch.com/prepaid-card-market. Accessed 23 October 2020.

-

Global Potential for Prepaid Cards. Edgar, Dunn & Company, 14 September 2019. edgardunn.com/wp-content/uploads/2019/09/Global-Potential-for-Prepaid-Cards-13092019.pdf. Accessed 23 October 2020.

-

“Coronavirus bailouts: Which country has the most generous deal?” BBC, 7 May 2020. www.bbc.com/news/business-52450958. Accessed 6 November 2020.

-

“Soldo Care Cards Help Governments, Local Authorities and NGOs Distribute Emergency Funds Amid COVID-19 Outbreak”. Soldo, 21 April 2020. www.prnewswire.co.uk/news-releases/soldo-care-cards-help-governments-local-authorities-and-ngos-distribute-emergency-funds-amid-covid-19-outbreak-838636253.html. Accessed 6 November 2020.

-

“The Number Of Disbursements Is Increasing, The Number Sent Instantly Barely Breaks 10 Percent”. PYMNTS.com, 8 September 2020. www.pymnts.com/disbursements/2020/new-data-the-number-of-disbursements-is-increasing-the-number-sent-instantly-barely-hits-10-percent/. Accessed 6 November 2020.

-

Earley, Kelly. “Prepaid Financial Services launches ‘spend local’ cards in Jersey”. Silicon Republic, 10 September 2020. www.siliconrepublic.com/companies/prepaid-financial-services-jersey-spend-local-cards. Accessed 6 November 2020.

-

Cornish, Chloe. “Iraq’s financial inclusion drive boosted by homegrown fintech”. Financial Times, 24 April 2019. www.ft.com/content/19b10528-4b36-11e9-bde6-79eaea5acb64. Accessed 6 November 2020.

-

“Kurdistan Region of Iraq (KRI) — Report on issuance of the new Iraqi ID card”. The Danish Immigration Service, November 2018. www.justice.gov/eoir/page/file/1111531/download. Accessed 6 November 2020.

-

“QI Card. About us”. Qi Card, 2020. qi.iq/english/about-us. Accessed 6 November 2020.

-

“Citymapper Mobility Index”. Citymapper, 2020. citymapper.com/cmi. Accessed 23 October 2020.

-

“IBM Study: COVID-19 Is Significantly Altering U.S. Consumer Behavior and Plans Post-Crisis”. IBM, 1 May 2020. newsroom.ibm.com/2020-05-01-IBM-Study-COVID-19-Is-Significantly-Altering-U-S-Consumer-Behavior-and-Plans-Post-Crisis. Accessed 6 November 2020.

-

Varella, Simona. “Italy: post-COVID car use frequency intentions 2020”. Statista, 24 June 2020. www.statista.com/statistics/1122994/post-covid-car-use-frequency-intentions-in-italy/. Accessed 23 October 2020.

-

“Enfuce powers payments in MaaS Global’s revolutionary mobility app”. Enfuce, 28 May 2020. enfuce.com/enfuce-powers-payments-in-maas-globals-revolutionary-mobility-app/. Accessed 6 November 2020.

-

“Cashless Transportation: Kenya and Rwanda As Case Studies”. Mondato, 1 January 2020. blog.mondato.com/cashless-transportation-kenya-rwanda/. Accessed 6 November 2020.

-

Ilako, Cynthia. “Kenya’s cashless public transport fails to pick, five years on”. The Star, Kenya, 2 January 2020. www.the-star.co.ke/business/kenya/2020-01-02-kenyas-cashless-public-transport-fails-to-pick-five-years-on/. Accessed 6 November 2020.

-

“Investor’s Information: FAQ”. MTR. www.mtr.com.hk/en/corporate/investor/investor_faq. Accessed 6 November 2020.

-

Tam, Adrian K. “Competition Heats Up in Hong Kong’s e-Payments Sector”. China Business Knowledge, 4 June 2020. cbk.bschool.cuhk.edu.hk/competition-heats-up-in-hong-kongs-e-payments-sector/. Accessed 6 November 2020.

-

“Business — Octopus Hong Kong”. Octopus, 2020. www.octopus.com.hk/en/business/index.html. Accessed 6 November 2020.

-

Reuters. “Argentina’s Mendoza province becomes first to pass law allowing Uber”. Reuters, 31 July 2018. www.reuters.com/article/idUSL1N1UR1NL.

-

Frosio, Giancarlo, and Vargas, Paula. “Argentinian Telecoms (and Credit Cards) Ordered to Block Uber App”. The Center for Internet and Society, 3 May 2016. cyberlaw.stanford.edu/blog/2016/05/argentinian-telecoms-and-credit-cards-ordered-block-uber-app. Accessed 6 November 2020.

-

BTCNN. “You Can Now Pay Using Bitcoin for a Uber Ride in Argentina”. Bitcoin News Network, 17 September 2018. www.btcnn.com/you-can-now-pay-using-bitcoin-for-a-uber-ride-in-argentina/. Accessed 6 November 2020.

-

Garrison, Cassandra. “Anti-Uber protests flare in Argentina as ride-hailing app prepares IPO”. Reuters, 11 April 2019. www.reuters.com/article/idUSKCN1RN1T0. Accessed 6 November 2020.

-

Szuc, Daniel. “A Really Smart Card: How Hong Kong’s Octopus Card moves people”. User Experience Magazine, 7 (4), 2008. Retrieved from uxpamagazine.org/really_smart_card/. Accessed 6 November 2020.

-

“2019 Annual Results of Octopus Cards Limited”. Octopus, 2020. www.octopus.com.hk/en/document/annual-accounts-announce-2019.pdf. Accessed 6 November 2020.

-

Statista Research Department. “Retail sales in the United States from 2012 to 2020, with a forecast until 2024”. Statista, 28 August 2020. www.statista.com/statistics/443495/total-us-retail-sales/. Accessed 23 October 2020.

-

“Starbucks Fiscal 2019 Annual Report”. Starbucks Corporation, 2019. s22.q4cdn.com/869488222/files/doc_financials/2019/2019-Annual-Report.pdf. Accessed 23 October 2020.

-

“Statistics at a Glance as of June 30, 2020”. The Federal Deposit Insurance Corporation, 2020. www.fdic.gov/bank/statistical/stats/2020jun/industry.pdf. Accessed 23 October 2020.

-

Garcia, Tonya. “No one does gift cards like Starbucks”. MarketWatch, 23 December 2015. www.marketwatch.com/story/why-almost-no-one-does-gift-cards-like-starbucks-2015-12-23. Accessed 23 October 2020.

-

“Starbucks Card FAQs”. Starbucks Coffee Company, 2020. www.starbucks.in/card/learn-more/card-faq. Accessed 23 October 2020.

-

Hinchliffe, Ruby. “Korean banks have growing concerns over Starbucks prepaid card”. Fintech Futures, 10 February 2020. www.fintechfutures.com/2020/02/korean-banks-have-growing-concerns-over-starbucks-prepaid-card/. Accessed 23 October 2020.

-

Bruene, Jim. “Starbucks Launches First Dedicated iPhone App for Stored-Value Cards”. Finovate Blog, 23 September 2009. finovate.com/starbucks_launches_first_mobile_stored_value_iphone_app/. Accessed 23 October 2020.

-

Wise Marketer Staff. “Multi-Tender Loyalty Earns the Attention of Starbucks”. The Wise Marketer, 25 September 2020. thewisemarketer.com/loyalty-strategy/multi-tender-loyalty-earns-the-attention-of-starbucks/. Accessed 23 October 2020.

-

“Starbucks Reports Record Q2 Fiscal 2018 Results”. Starbucks Corporation, 26 April 2018. s22.q4cdn.com/869488222/files/doc_financials/quarterly/2018/q2/Starbucks-Q2-FY18-Earnings-Release.pdf. Accessed 23 October 2020.

-

Webster, Karen. “Why Invisible Will Make 2020’s Payments Innovation Roar”. PYMNTS.com, 3 September 2019. www.pymnts.com/news/payments-innovation/2019/why-invisible-will-make-2020s-payments-innovation-roar/. Accessed 23 October 2020.

-

Business Wire. “Starbucks and Chase Introduce Starbucks Rewards™ Visa® Prepaid Card”. Business Wire, 11 June 2018. www.businesswire.com/news/home/20180611005230/en/Starbucks-and-Chase-Introduce-Starbucks-Rewards%E2%84%A2-Visa%C2%AE-Prepaid-Card. Accessed 23 October 2020.

-

“Costa Coffee and Barclaycard launch UK’s first contactless reusable “clever cup”. Barclaycard, 28 November 2018. www.home.barclaycard/media-centre/press-releases/Costa-Coffee-and-Barclaycard-launch-UKs-first-contactless-reusable-clever-cup.html. Accessed 6 November 2020.

-

“Costa Coffee launches contactless reusable cups”. Finextra, 19 November 2018. www.finextra.com/newsarticle/32965/costa-coffee-launches-contactless-reusable-cups. Accessed 6 November 2020.

-

Peyton, Antony. “Barclaycard wakes up to Costa Coffee’s contactless cup”. FinTech Futures, 19 November 2018. www.fintechfutures.com/2018/11/barclaycard-wakes-up-to-costa-coffees-contactless-cup/. Accessed 6 November 2020.

-

Cramer, Harriet. “Costa Coffee and Barclaycard launch contactless reusable Clever Cup”. FMBE, 28 November 2018. fieldmarketing.com/news/costa-coffee-barclaycard-lunch-contactless-reusable-clever-cup/. Accessed 6 November 2020.

-

Maytom, Tim. “Costa Coffee and Barclaycard team up for contactless ‘Clever Cup’”. Mobile Marketing, 28 November 2018. mobilemarketingmagazine.com/costa-coffee-and-barclaycard-team-up-for-contactless-clever-cup. Accessed 6 November 2020.

-

Loukil, Alexandre. “Carrefour va supprimer son offre bancaire C-zam et propose un compte Nickel en échange”. Capital, 13 May 2020. www.capital.fr/votre-argent/carrefour-va-supprimer-son-offre-c-zam-et-propose-un-compte-nickel-en-echange-1369935. Accessed 6 November 2020.

-

Sergeur, Frédéric. “Carrefour veut-il abandonner sa banque en ligne C-Zam ?” Capital, 11 October 2019. www.capital.fr/entreprises-marches/carrefour-veut-il-abandonner-sa-banque-en-ligne-c-zam-1352628. Accessed 6 November 2020.

-

Baker, Talie. “U.S. Payroll Card Market Overview: The State of Pay”. AiteGroup, 7 September 2017. www.aitegroup.com/report/us-payroll-card-market-overview-state-pay. Accessed 6 November 2020.

-

Yuan, Melody. “Advantages of Using Prepaid and Payroll Cards for Touchless Money Disbursement and Management”. Reach Further by East West Bank, 14 September 2020. www.eastwestbank.com/ReachFurther/en/News/Article/Advantages-of-Using-Prepaid-and-Payroll-Cards. Accessed 6 November 2020.

-

Champagne, Jesse. “The Rise of The Gig Economy: How Electronic Payments Can Help Pt. 1”. Finextra, 28 March 2019. www.finextra.com/blogposting/16904/the-rise-of-the-gig-economy-how-electronic-payments-can-help-pt-1. Accessed 6 November 2020.

-

“Pleo – How it works”. Pleo Technologies Ltd, 2020. www.pleo.io/en/howitworks. Accessed 6 November 2020.

-

Essén, Linda. “Collaboration between Enfuce and Pleo”. Enfuce, 15 November 2019. enfuce.com/nordic-fintech-startups-enfuce-and-pleo-collaborate-to-accelerate-expansion-into-europe/. Accessed 6 November 2020.