Omnichannel commerce isn't just the future of retail — it's the present reality for merchants everywhere. The pandemic accelerated this shift, prompting businesses to rapidly expand onto new social platforms, websites, and virtual touchpoints to engage customers through fluctuating restrictions. From online shopping sprees to in-store experiences, consumers now demand a seamless transition between digital and physical realms, expecting the same fast, convenient, and personalized interactions across all channels. Companies with omnichannel customer engagement strategies retain on average 89% of their customers. In contrast, companies with weak omnichannel customer engagement have a customer retention rate of only 33%, according to data from Invesp.

Both online merchants branching into physical stores and traditional retailers venturing into the digital realm encounter similar hurdles. They need to provide the same experience across all touchpoints — be it purchasing, returning items, providing feedback, or accessing promotions. Simply having multiple channels isn't sufficient; the challenge is to navigate the dynamic ways customers engage and ensure cohesion across them all. And as businesses grow, reconciling data from disparate channels adds another layer of complexity.

.png?width=1913&height=661&name=1+(2).png)

In this article, OpenWay, a top digital payments platform provider, shares insights from successful omnichannel players, including its clients Nexi and Shift4 in Europe, Equity Bank in Africa, Banesco Panama in Latin America, Halyk Bank and SmartPay in Asia, and others. We delve into the distinctions between omnichannel and multichannel approaches, the challenges businesses confront during the transition, and the strategic and technological tactics underpinning a thriving omnichannel strategy.

Where did omnichannel come from? How is it different from multichannel?

Omnichannel has been around for over a decade. The idea of starting interactions from one point, say, a website, and concluding them at a physical pickup location, is simple and familiar to most people who don’t expect a huge difference between online and physical stores. But when the word “omnichannel” was coined, the average consumer used only two touchpoints per purchase. In 2019, the number of average touchpoints for a consumer was reported to be six. Since the pandemic, many merchants quickly added new offerings to survive and then thrive. Curbside pickup, contactless and mobile wallets, BNPL payment choices online and in-store … the customer journey came to encompass more and more touchpoints across multiple channels.

Now more than ever, merchants find that they need to consider the various channels their customer journey might include and what they look like from a customer point of view. Even if the destination is the same, is each channel a separate highway, passing through a completely different landscape? If so, no matter how much traffic each highway contains, what we have is multichannel, but not yet omnichannel.

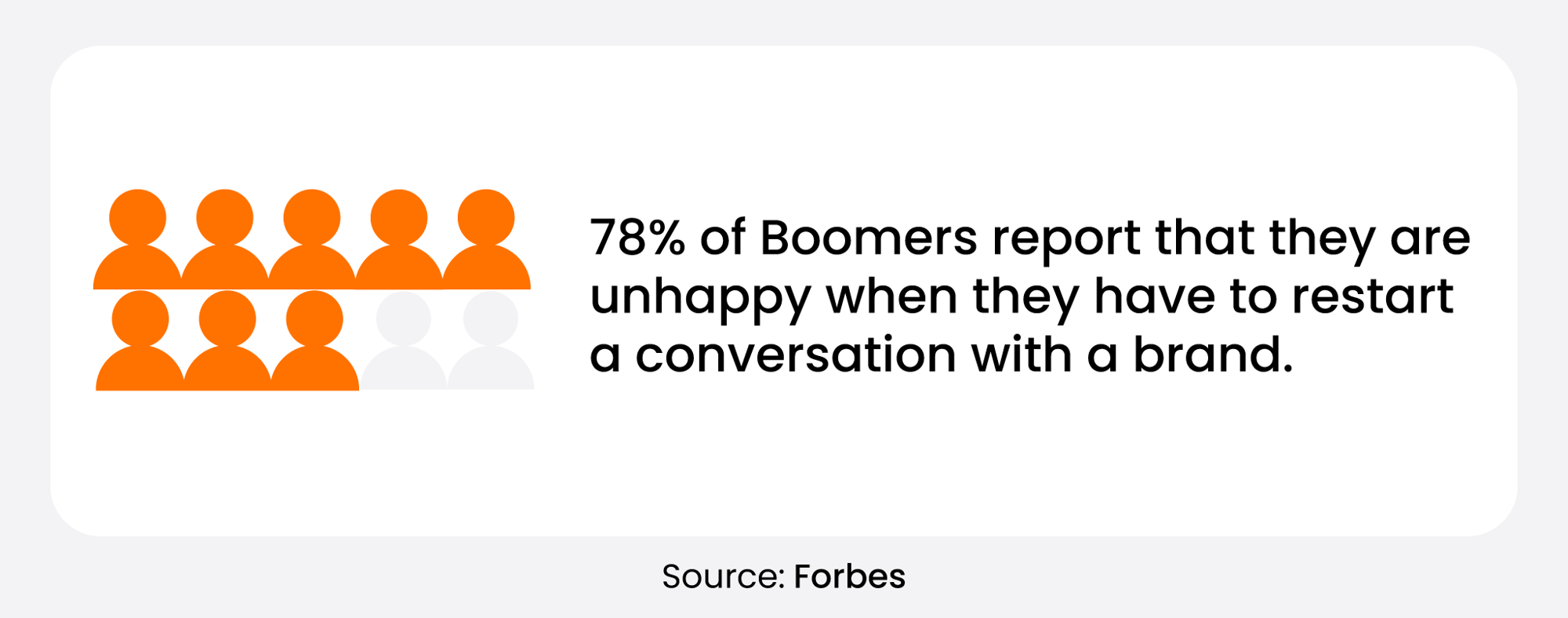

So what is the difference? Multichannel focuses on making each channel as pleasant and attractive as possible for customers, measuring success in terms of engagement such as likes and views, and how conveniently and effectively customers can shop and checkout. Each channel is its own separate customer journey. If a customer wants to switch channels, he or she may need to start again, re-registering at worst and repeating a selection at best.

Omnichannel, on the other hand, is all about an integrated, smoothly fluid customer journey where the customer has a single view of the company and can choose any channel to communicate with a brand. More than one channel can be used to initiate, modify and complete a transaction and the journey will be seamless and consistent, meaning that customers can naturally transition from one platform to another and expect that all their previous interactions with the brand or company are accessible from there. And regardless of the channel used, customers want to feel like they are engaging with the same entity at all times.

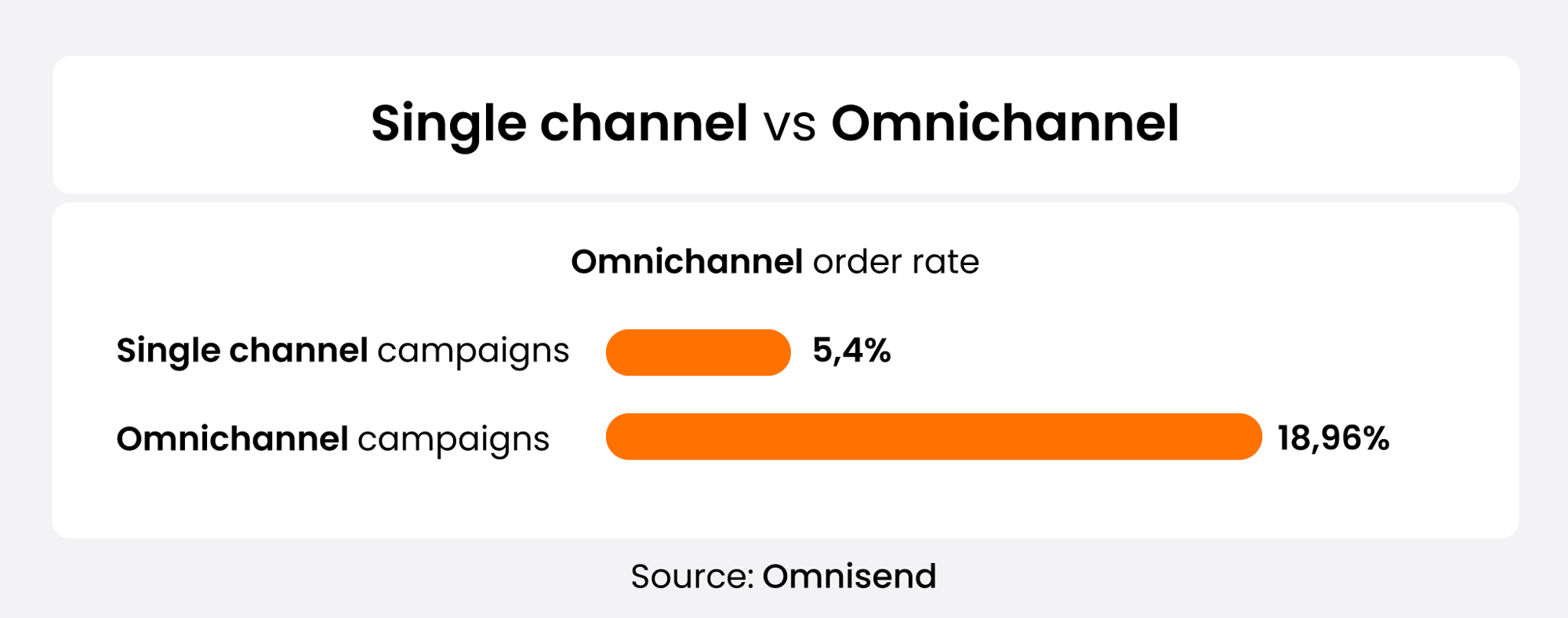

So that’s the customer view of omnichannel. What about the merchant’s? From their perspective, it starts with a consistent customer identity – recognition of a customer’s device, an ID or token, needed for cross-platform customer data management and security. Omnichannel is all about seamless payments, for which the where, the when and the how are entirely up to the customer. And more often than not, this is what people expect. According to one study, 90% of customers expect their interactions to be consistent across all channels. And even before the pandemic, single-channel campaigns showed a 5,4% engagement rate, while omnichannel campaigns enjoyed 18,96%.

What challenges stand in the way of true omnichannel?

It might be said of omnichannel that “if it was easy, everyone would be doing it”. Although the pandemic succeeded in driving many businesses to a multichannel approach, several factors prevent them from becoming truly omnichannel.

-

Separate online and offline operations, disparate POS and e-checkout systems. The data coming from separate online and offline systems are siloed, inconsistent, and cannot be used across various channels and platforms. For example, customers starting their transactions online cannot continue offline, and vice versa.

-

Consumer privacy and security issues increase as more and more parties process data. Omnichannel depends on huge pools of data collected from digital channels such as social media, chat, mobile apps and websites. For all this to make any sense, merchants can rely on secure, cross-platform customer identity management systems. However, if customers still see inconsistencies in the way a retailer’s online platform processes their data, such as unexpected requests for login or problems during onboarding and ID verification, they may opt out. According to one survey, nearly 92% of consumers had uninstalled a retail app over privacy concerns.

-

Difficulties in consolidating data, inheritance of different legacy systems. As merchants expand, they may acquire new platforms and channels that cannot be fully reconciled with existing ones, each with its own type of data, implementation and support. Onboarding, multi-currency, risk rules and special services may be handled by separate systems, meaning there is no unified conversion and integration of data. But this integration is essential for consumers to get unified access to their payment methods, preferences, history and social media accounts in a seamless experience.

What are the components of a successful omnichannel strategy?

1. Deliver a unified and coordinated digital performance

Regardless of the diversity of a company's touchpoints and engagement methods, its ability to adapt and integrate diverse elements is crucial. To achieve this, a unified, consistent digital model and set of business rules should govern all digital and physical channels, accommodating the unique characteristics of each and their combinations throughout a customer's journey. Failure to meet this challenge with digital capabilities can lead to customer frustration.

Nexi, an OpenWay client, aimed to enhance merchant experiences by introducing various services such as personalized dynamic pricing and expediting the time-to-market for new acquiring services. Despite the start of the pandemic, Nexi decided to replace several legacy acquiring systems with a single, flexible omnichannel platform that would enable its extensive portfolio of one million merchants to thrive within a unified system. OpenWay's Way4 acquiring platform was successfully implemented within nine months, regardless of pandemic restrictions. Since then, Nexi’s acquiring customer base has grown to 2 million. They also have become the largest acquirer in Europe in terms of number of merchants served and overall transaction value handled!

When acquirers have to manage disparate technological platforms, providing the same rules and experiences may be a challenge across different merchant segments. With a unified back end on a single platform, merchants are able to give their end customers the same, predictable experiences at checkout according to a unified set of rules and defined scenarios across all channels.

“Way4’s system architecture allows us to centrally manage all our operations, launch innovations and sustain transaction volume growth”.

Nexi’s ability to support consistent acceptance is not limited to international payment schemes – it also encompasses domestic schemes such as the popular Bancontact debit card in Belgium and the iDEAL payment system in the Netherlands.

Mirroring this technological centralization, the teams responsible for operations on the acquirer side will benefit from streamlining their internal and external communications. Various groups may be handling different components of a single customer journey both online and offline, encompassing logistics, order processing, delivery as well as onboarding and account management. Management of these business processes involves maintaining a highly flexible and efficient workflow. Teams that understand the specifics of each channel and apply insights gleaned from customer data can better deliver the experiences expected from them. If communication is coordinated between marketing, sales, customer service, and other departments, merchants will receive a clear, consistent overview of their activity at all times.

2. Collect and effectively use customer data to understand behavior

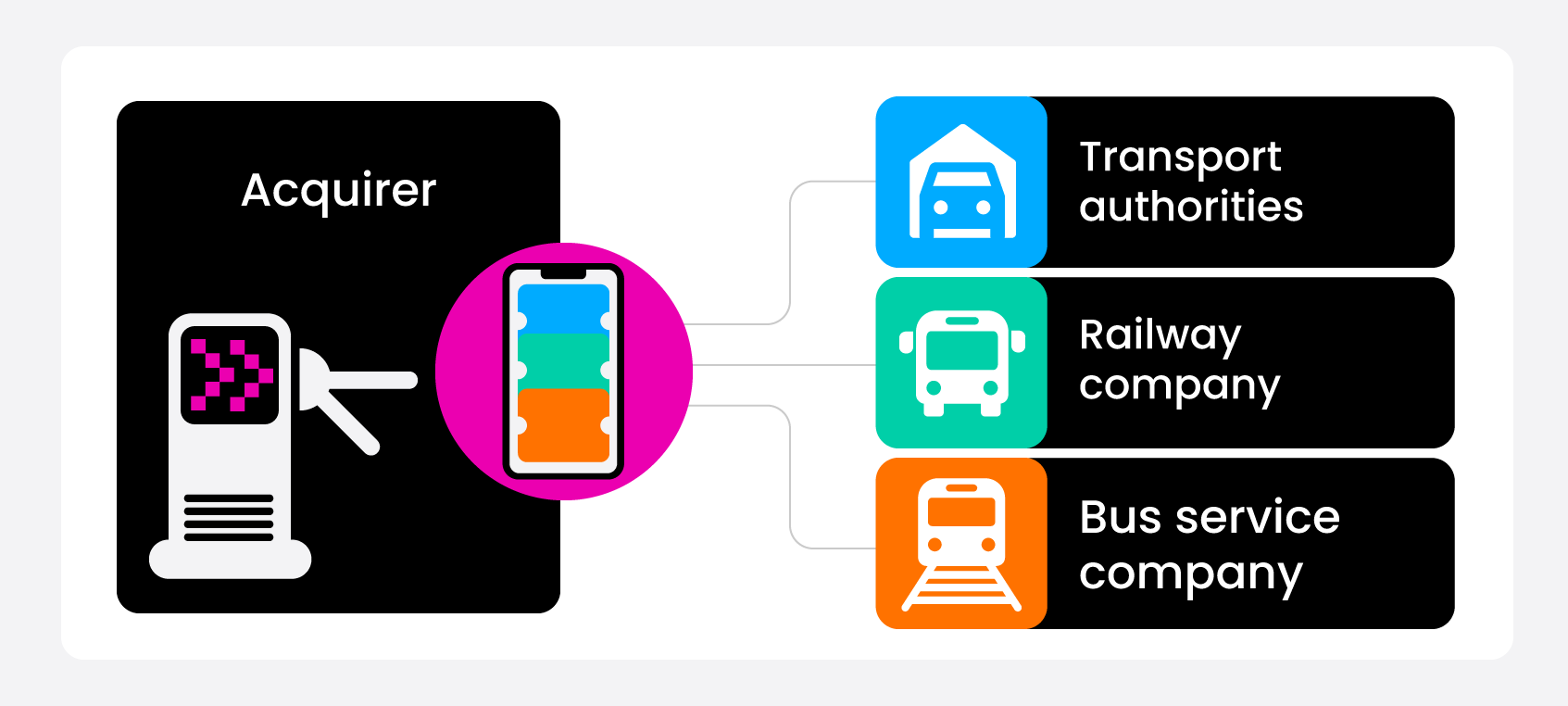

The more data an acquirer is able to accumulate and share, the easier it becomes for its merchants to enhance their service quality and efficiency. For instance, one of our clients implemented contactless card payment systems on suburban railway lines, offering passengers the convenience of paying transit fares on turnstiles and upgrading their ticket class to business. In such endeavors, the transaction data captured by Way4, including details on location, amount, and frequency per passenger, provides valuable insights for stakeholders such as the railway company and public transport planning authorities, and improve their decision-making.

As the number of payment acceptance channels increases, merchants may find themselves requiring more and more sophisticated data. They may need to know: how frequently do customers interact with each channel and through which devices? What is the overall impact of these interactions? To get answers, merchants not only need access to a fully integrated tech stack capable of getting the necessary data, they may also need additional tools for deep data analysis. This includes processing of Level 3 data, data streaming, CRM tools, and acquiring profitability tools. Cross-platform customer identity management, mentioned earlier, can help make sure that all the disparate behaviors are tied to specific customers, enabling profiles to be developed. It is important that data collection and analysis is done regularly and in a timely manner. According to one study, 60% of customer identity data is no longer relevant after two years.

OpenWay’s Way4 platform is used by acquirers to collect diverse channel and transaction data and stream it to an online self-service portal: the Way4 Merchant Portal. It offers merchants a comprehensive view of each cardholder’s transaction history across various payment channels, including transaction amounts and itemized purchases. This data can be seamlessly integrated into merchants’ external analytic and reporting systems for deeper insights.

One crucial feature of Way4 is its ability to capture line items during transactions, particularly essential for fleet acquirers. This enables real-time validation of whether a fleet driver is authorized to purchase products from specific categories like fuel or food with the payment card provided by the fleet company. Any unauthorized transactions are swiftly identified and rejected. Moreover, Way4 dynamically analyzes both Level 2 and 3 data, adjusting authorization algorithms in real time regardless of the payment channel utilized by the driver.

3. Based on the data, map service journeys with design thinking

So, we have done a great job collecting and analyzing the data. Now we need to work further to collate it into defined end-to-end customer journeys. Although identifying the most frequently used touchpoints is important, it would be a mistake to channel all company resources to improving them without understanding what role they play in the overall customer journey. Moreover, since omnichannel is increasingly cross-border as well as cross-platform, ethnographic research may be necessary to analyze specific behaviors and preferences of various segments. Once a new customer journey has been developed, design thinking and rapid testing with customer groups will help make any needed adjustments and roll it out quickly.

One company that took improvement of customer journeys seriously is OpenWay client Shift4 in Europe, who provides omnichannel payments to over 200,000 merchants globally, including such well-known brands as Starlink, Hilton, Kiwi, Wolt and Xsolla. It was one of the first e-commerce acquirers to identify the gap in multi-currency services and launch MCP (multi-currency pricing) service. Now it supports acceptance in 160+ currencies and settlement in 25+ currencies to guarantee the convenience of paying in local currency for the customer, on one hand, and the optimized FX rates and simpler reconciliation for merchants, on the other.

To incentivize selected merchants, acquirers can offer to split the markup on FX conversion rates. Such profit-sharing agreements may be a true competitive advantage in cross-border acquiring. Way4 supports this model by automating the accounting, billing, and reporting workflows related to the markup splitting.

As another global advantage, Shift4 offers one of the highest approval rates in the e-commerce industry. To achieve this, the acquirer has developed a unique methodology which involves monitoring of spikes and drops in the approval rate, analyzing rejection patterns per card type, merchant, channel, and other parameters, and making the necessary adjustments in the processing system. Among the factors influencing the transaction success, Shift4 continues to optimize authentication and payment methods. It provides merchants with valuable insights on which of these methods could be offered to customers based on region- and vertical-specific requirements and emerging trends.

In certain industries, creating a seamless payment experience presents significant challenges. Take fleet acquiring, for instance, where there are numerous payment pathways. Consider a scenario where a driver opts to pay for fuel directly at the pump, then decides to make an additional purchase inside the station's store, settling the payment at a regular POS terminal. Alternatively, the driver might defer payment at the pump and choose to pay inside the store for both fuel and snacks. Furthermore, the payment workflow at the pump can vary, even within the same gas station chain. Stations equipped with a store may feature pump payment screens showcasing various available goods. If there's an adjacent car wash, the pump workflow might incorporate payment options for this additional service. Conversely, at fuel-only stations, drivers prefer straightforward payment instructions with minimal additional information displayed on the screen. Navigating these diverse payment scenarios requires meticulous attention to detail and flexibility in accommodating varying preferences and circumstances.

As acquirers accumulate more and more data from all their merchants, they are in a position to identify trends about which payment channels or methods have the highest conversion. These insights are valuable to merchants who can decide which payment method could be offered to their customers at what stage of their journey. Consumers are more likely to stick to the checkout process to the end when they know that they can pay in a way that is most convenient for them, resulting in higher conversion rates. Acquirers must be vigilant about accommodating emerging payment channels, which evolve rapidly. For example, among card-not-present channels, Pay By Link is indisputably on the rise, Moto is still popular in regions like Canada, and e-commerce QR code checkout is enabling retailers to make checkout faster and more convenient around the world.

4. Give merchants and their customers convenient control over payment channels and methods

What combination of factors makes a certain payment method desirable and convenient depends on the customer and the overall experience. Cash, check, bank transfers, debit and credit cards, mobile wallets, Buy Now, Pay Later, prepaid cards…all these options are important to various generations of customers in a variety of situations. Moreover, new payment preferences evolve over time. Among OpenWay clients are many acquirers who started their business with one segment or channel, then expanded to encompass others in accordance with the expanding payment needs of merchants and their target buyers. For example, Halyk Bank of Kazakhstan chose to migrate to the Way4 platform while it was becoming the leading POS acquirer in its region. Then, the bank launched e-commerce acquiring on the same platform, and when it had become the top e-commerce acquirer, it launched QR payments for SME. The speedy launch and success of these merchant offerings was greatly facilitated by its new digital payments platform, which uses single set of data and business rules.

Even in countries with a large unbanked population, more than one payment channel may be welcomed and adopted by merchants. For example, OpenWay client SmartPay in Vietnam started with C2B (consumer to business) payments as a mobile transfer within a mobile wallet ecosystem based on its popular app. Next, they added acceptance of QR code payments for both old and new merchants. Today, SmartPay services 700,000 merchants who rely on mPOS and digital wallet acceptance channels, and over 40 million consumers who embrace these convenient payment methods.

Vietnam is not the only country where the concept of wallet-based marketplace may thrive. This business model is also attractive for Banesco Panama, an OpenWay client in Central America. Today, the company has the largest number of POS in the acquiring market of Panama and is focused on e-commerce, which grew significantly during the pandemic and has continued its trajectory in development. Banesco Panama is also looking into the digital wallet as a marketplace to manage many transactions on a single device. The ability to provide a seamless experience throughout various payment offerings will undoubtedly contribute to building greater loyalty and improving the customer experience.

What’s next?

If your organization seeks to offer omnichannel capability through a robust acquiring platform, we warmly invite you to explore Way4. Trusted by acquirers worldwide, Way4 stands out for empowering both acquirers and their merchants with seamless omnichannel experiences, all orchestrated on a single platform with a unified set of rules and data management. It is the only one on the market to boast an online acquiring front- and back- -office, allowing acquirers to flexibly configure business rules and effortlessly access real-time data. Successful omnichannel payment models embraced by OpenWay clients include POS, e-commerce, mobile payments, digital wallets, national payment systems, instant payments and instant settlements, BNPL, cross-border payments, fleet solutions, and more.

With unmatched scalability, the Way4 digital payments platform supports acquiring businesses ranging from thousands to millions of merchants within a single deployment. OpenWay offers flexible deployment options for Way4, both on-premise and in the cloud. Additionally, it offers an expedited Way4 SaaS solution through certified SaaS operational partners, where deployment is completed in a matter of months.

If you want to learn how OpenWay solutions can support your acquiring business, please contact us. Our team will be happy to analyze your needs and show you how Way4 can elevate your omnichannel aspirations!

![OW 11 [Flexible by design]](https://openwaygroup.com/hubfs/Partners%20portal/Logos%20and%20icons/OW_Logotype_RGB_99x28_s2.png)

OpenWay is the only best-in-class provider of digital payment software solutions for card issuing, digital wallets, merchant acquiring, BNPL, transaction switching, tokenization, and fleet payments, and the best cloud payment systems provider as rated by Aite, PayTech and Juniper Research. Top-tier banks and processors, as well as ambitious fintech startups, have chosen OpenWay as their strategic partner. With its unique capabilities in rich functionality, fast-to-market, high availability and better ROI, the Way4 software platform guarantees an unparalleled customer payment experience.