Battle of cards and wallets?

Mobile payment transaction volumes in the US is projected to grow steadily and to match the worldwide pattern. Source: The State of Mobile Payments in 2019. New ETA Report.

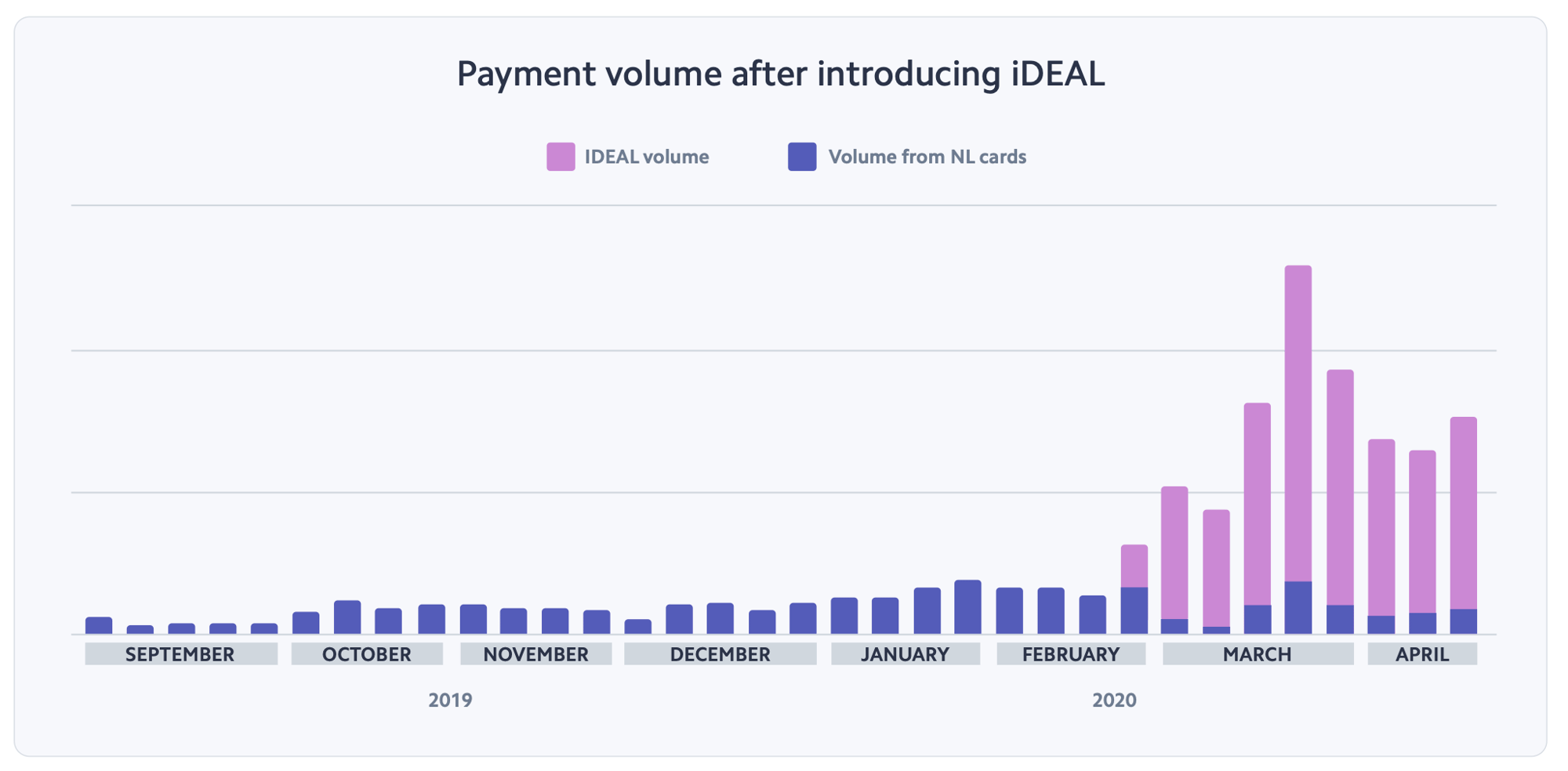

In Belgium, a popular domestic mobile wallet for online, in-store and P2P transactions is Payconiq by Bancontact. The speed of its adoption is promising. In 2018 it processed 34 million mobile payments – an increase of 100% compared with the previous year. By July 2019, over 60,000 merchants across the Benelux region have connected to the Payconiq wallet platform.

Still, the Payconiq ecosystem in Belgium has a weakness: lack of acceptance in physical stores. Although the Payconiq mobile app supports QR code payments, they are rarely enabled by offline merchants within the country. Mobile NFC is supported, but only by the app’s Android version.

OpenWay is a best-in-class provider of digital payment software solutions, and the best cloud payment systems provider as rated by Aite and PayTech. OpenWay is a strategic partner of tier 1/2 banks and processors, fintech startups, and other leading payment players around the globe. Among them are Network International and Equity Bank Group in MENA, Lotte and JACCS in Asia, Nexi and Shift4 in Europe, Comdata (a Corpay Company) and Banesco in Americas, and Ampol in Australia.