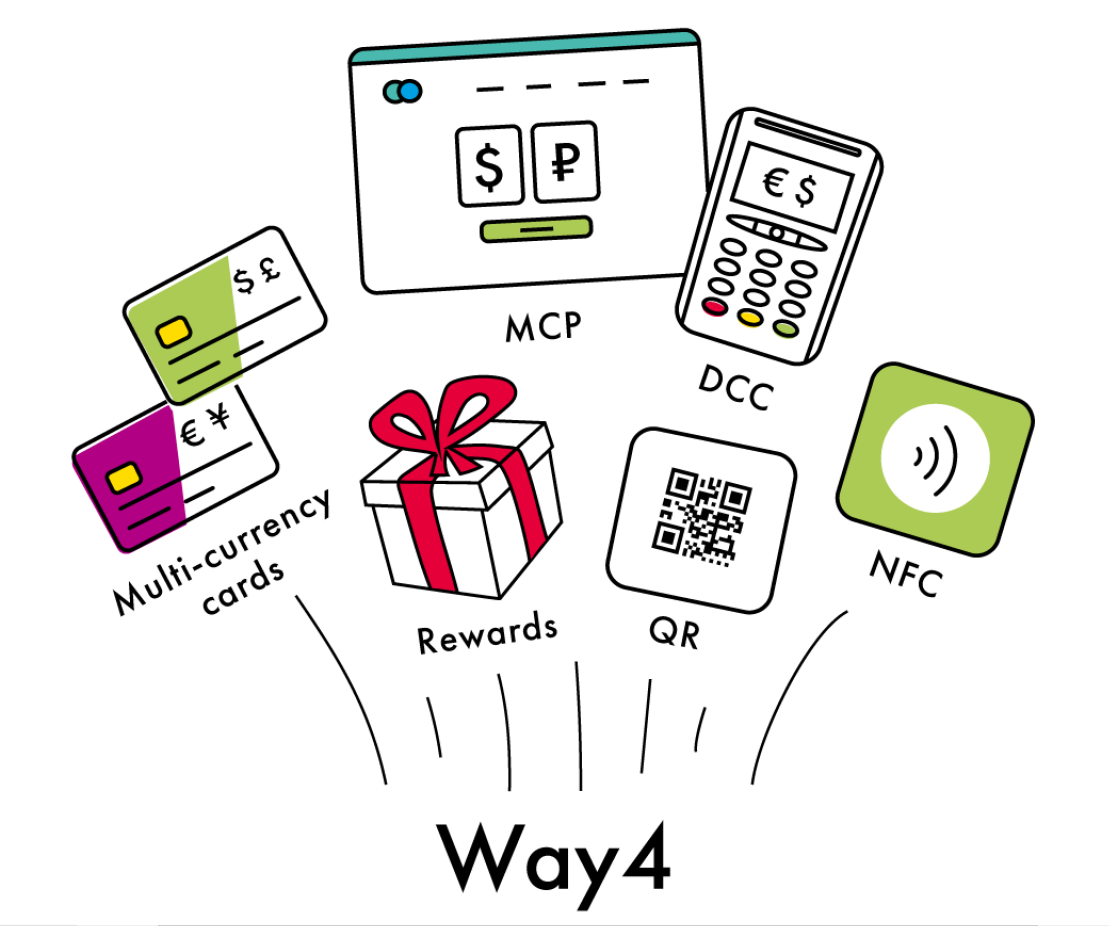

Alright, let's not sweat over multi-currency cards and payments

Meet the author

The exchange rate for KZT (Kazakhstan tenge) to EUR was chaotic and unpredictable all year in 2015.

From time to time clients and partners visit me in our Belgian headquarters, but more often I travel to their offices instead. Not all of my trips are within Europe. There are dozens of countries around the world, from the US to Indonesia, where I go and can’t help worrying about currency exchange. How much cash should I withdraw to pay for a taxi? What conversion rate is used in the hotel where I am staying?

Could my bank help me worry less about travel expense management? Corporate multi-currency cards, with a good exchange rate and low cash withdrawal fees, tick all the boxes. They are convenient for making business purchases in a foreign currency. They allow businesses to save money and also give peace of mind to the traveling employees. It seems too good to be true, but such cards really do exist. Our client Enfuce, a global cloud-based payment processor, is one such issuer.

If the corporate multi-currency card is powered by our WAY4 solution, then it can recognize exactly what I am buying in real-time. It allows payments only for certain product categories and within spending limits which my company defines. The limits can be unique for each corporate card or each department, or the same for all the employees.